I. Annual Production Review

MHP:

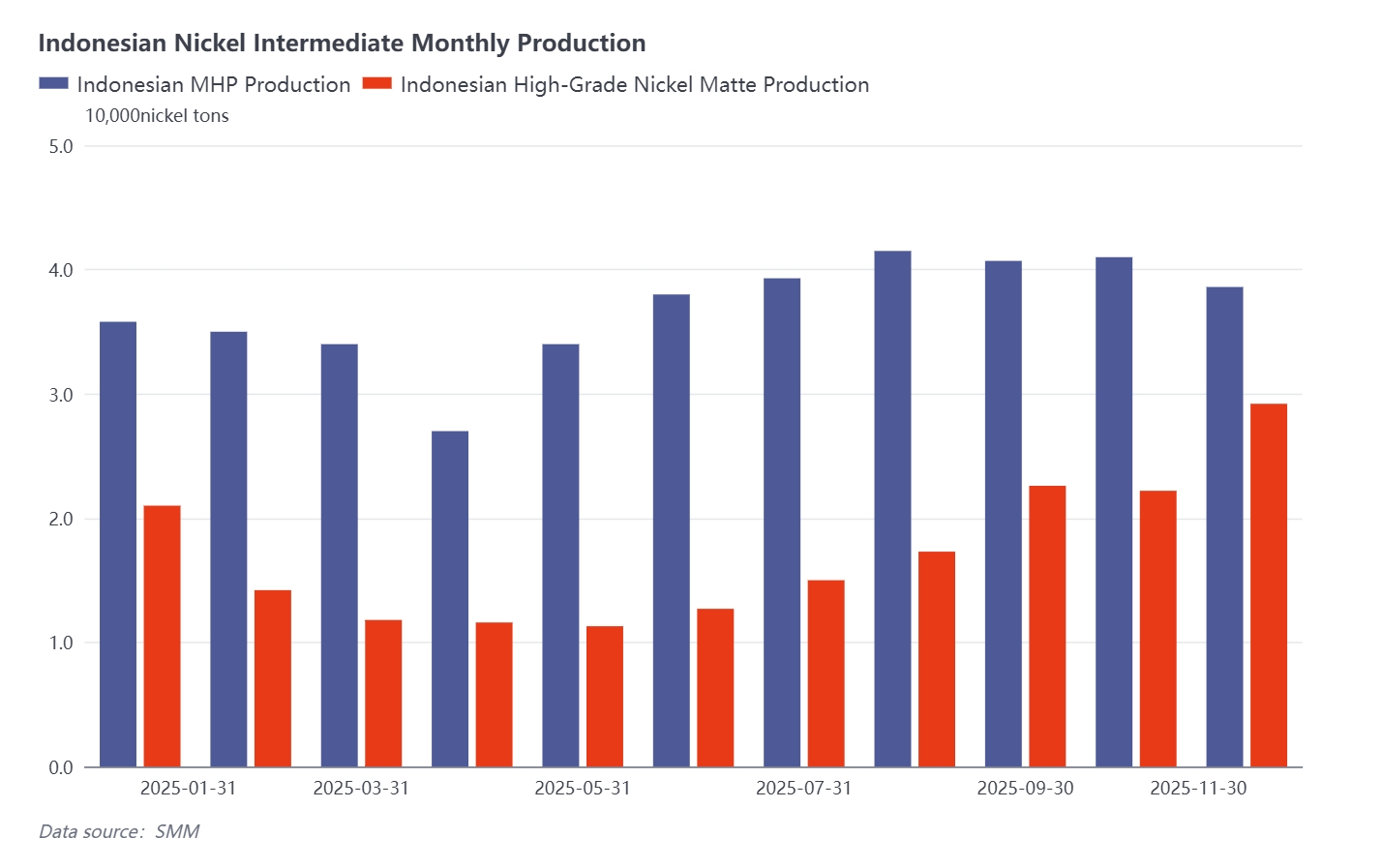

Full-year 2025 production increased YoY, with new project capacity of 20,000 mt Ni. Full-year production is currently projected at 445,500 mt Ni, up 36.6% YoY. By quarter, in Q1, MHP project output was affected by traditional holidays in China and Indonesia, leading to a lower operating rate and a month-by-month decline in production. In Q2, some Indonesian MHP projects were impacted by flooding, causing a significant drop in April output, which gradually recovered thereafter. In Q3, production rose, with some Indonesian MHP projects exceeding targets and increasing output; however, maintenance at some MHP projects in September, along with production cuts at others, led to a slight decrease. In Q4, some MHP projects remained under maintenance, combined with rectifications at certain Indonesian MHP projects, resulting in an overall production decline.

High-Grade Nickel Matte:

Full-year 2025 production decreased YoY, with new project capacity of 101,000 mt Ni. Full-year production is currently projected at 218,500 mt Ni, down 20.3% YoY. By quarter, in Q1, high-grade nickel matte was constrained by high costs and low price acceptance, compounded by profit competition with NPI, leading some producers to halt conversion and a significant drop in output. In Q2, the shutdown trend at some production lines continued, causing a slight decline. In Q3, due to increased new energy orders for some smelters, the production schedule for high-grade nickel matte rose. Coupled with the commissioning of new projects, overall Indonesian high-grade nickel matte production increased. In Q4, due to low acceptance of high payables of MHP and tight supply-demand conditions, some high-grade nickel matte lines resumed production, leading to a noticeable output increase.

II. Full-Year Price Review

MHP:

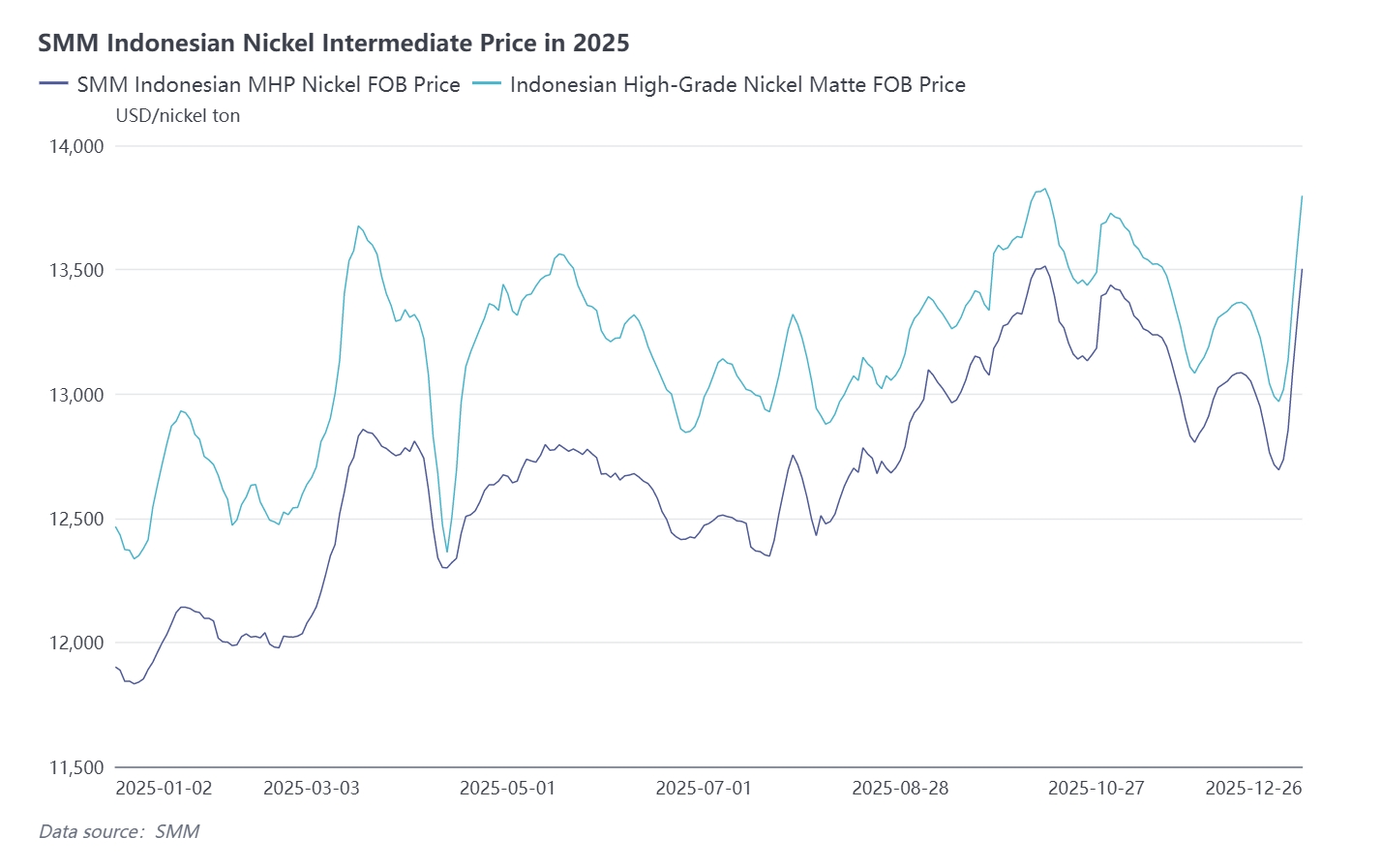

Prices fluctuated upward throughout 2025, ranging between $11,800-13,500/mt Ni. The peak reached $13,514/mt Ni in October, while the low was $11,833/mt Ni in early January. In Q1, the suspension of some high-grade nickel matte production lines led some nickel salt and refined nickel plants, which previously used high-grade nickel matte as raw material, to switch to MHP as an alternative. This increased MHP demand, and coupled with stimulus from Indonesia's macro policies, LME nickel prices also saw a slight rise, lifting MHP's final price. In Q2, April saw a reduction in MHP production due to floods in Indonesia. The weakened MHP supply pushed up MHP payable. However, US tariff policies caused a significant drop in LME nickel price, preventing a substantial rise in the final price. In Q3, August entered the traditional September-October peak season. Although LME nickel price declined under macro pressure and weak fundamentals, the final price still showed an overall upward trend, supported by rising MHP payable. In Q4, downstream new energy demand remained in the peak season, and cobalt intermediate product supply tightened due to the DRC, prompting some cobalt sulphate plants to increase MHP purchases. Driven by demand, MHP payable rose. However, expectations for a "hawkish" monetary policy boosted the US dollar, and high market inventory pressure led LME nickel price to fluctuate downward, causing a decline in MHP's final price.

High-Grade Nickel Matte:

Prices fluctuated upward throughout 2025, ranging between $12,300-13,900/mt Ni. The peak reached $13,826/mt Ni in October, while the low was $12,336/mt Ni in January. In Q1, the cessation of conversion at some high-grade nickel matte production lines reduced supply, pushing up payable. Combined with stimulus from Indonesia's macro policies, which led to a slight rise in LME nickel price, the fina price of high-grade nickel matte increased. In Q2, persistently tight market supply supported higher payable. However, LME nickel price declined due to weakened expectations for US Fed interest rate cuts and weak fundamentals, causing the final price of high-grade nickel matte to rise in April before slowly falling. In Q3, tight spot supply led some traders to raise offers, and downstream enterprises showed increased acceptance of high-payable raw materials, driving high-grade nickel matte payable higher. Nevertheless, dragged down by falling LME nickel price, the final price of high-grade nickel matte rose amid fluctuations. In Q4, downstream new energy demand remained in the peak season, and tradable resources in the market were scarce. Demand-driven increases in payables were offset by a stronger US dollar due to expectations for a "hawkish" monetary policy and high market inventory pressure, leading LME nickel price to fluctuate downward and causing a decline in the final price.

III. Economic Competition of Raw Materials

MHP vs. High-Grade Nickel Matte:

Comparing MHP and high-grade nickel matte, first, in terms of ore supply stability, current pyrometallurgical ore reserves in Indonesia last for about 10 years, while hydrometallurgical ore reserves last for 20–30 years. Due to the stability of ore production, enterprises prefer MHP as a raw material to ensure stable production. Second, economically, integrated enterprises currently find it more cost-effective to process MHP as a raw material compared to high-grade nickel matte. Third, on the supply side, MHP continues to increase in volume, and the resulting surplus leads to lower prices, enhancing its economic appeal. Fourth, MHP contains cobalt, which, under the current DRC quota policy, makes it an indispensable alternative raw material.

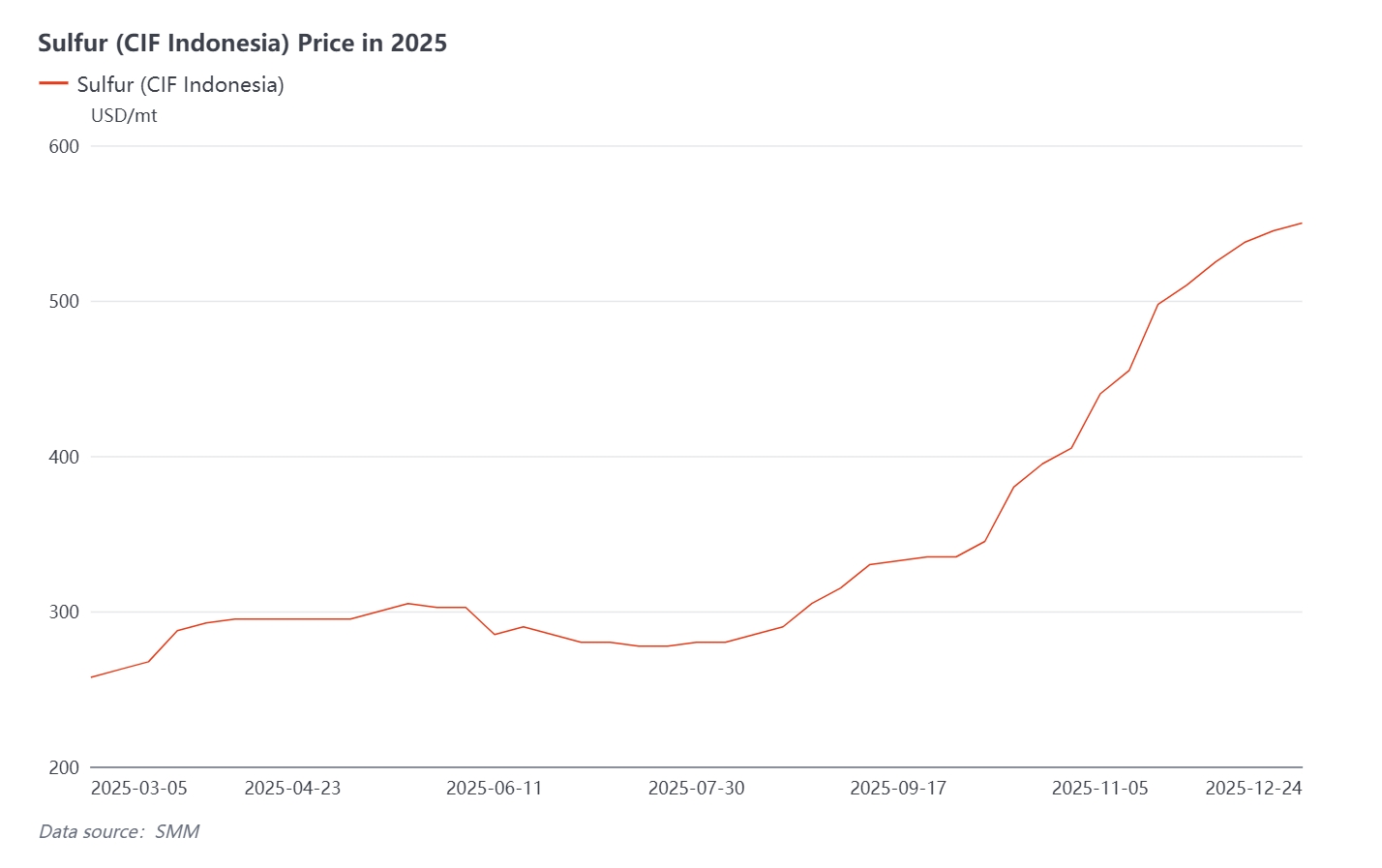

Important risk note: The price of sulfur has now exceeded $530/mt, accounting for 29% of MHP production costs. If sulfur prices continue to rise, the production economics of MHP and high-grade nickel matte may shift.

NPI vs. High-Grade Nickel Matte:

As a product of NPI conversion, smelters compare the profit margins from selling NPI and high-grade nickel matte as raw materials and independently decide whether to proceed with conversion.

IV. Annual Cost Review

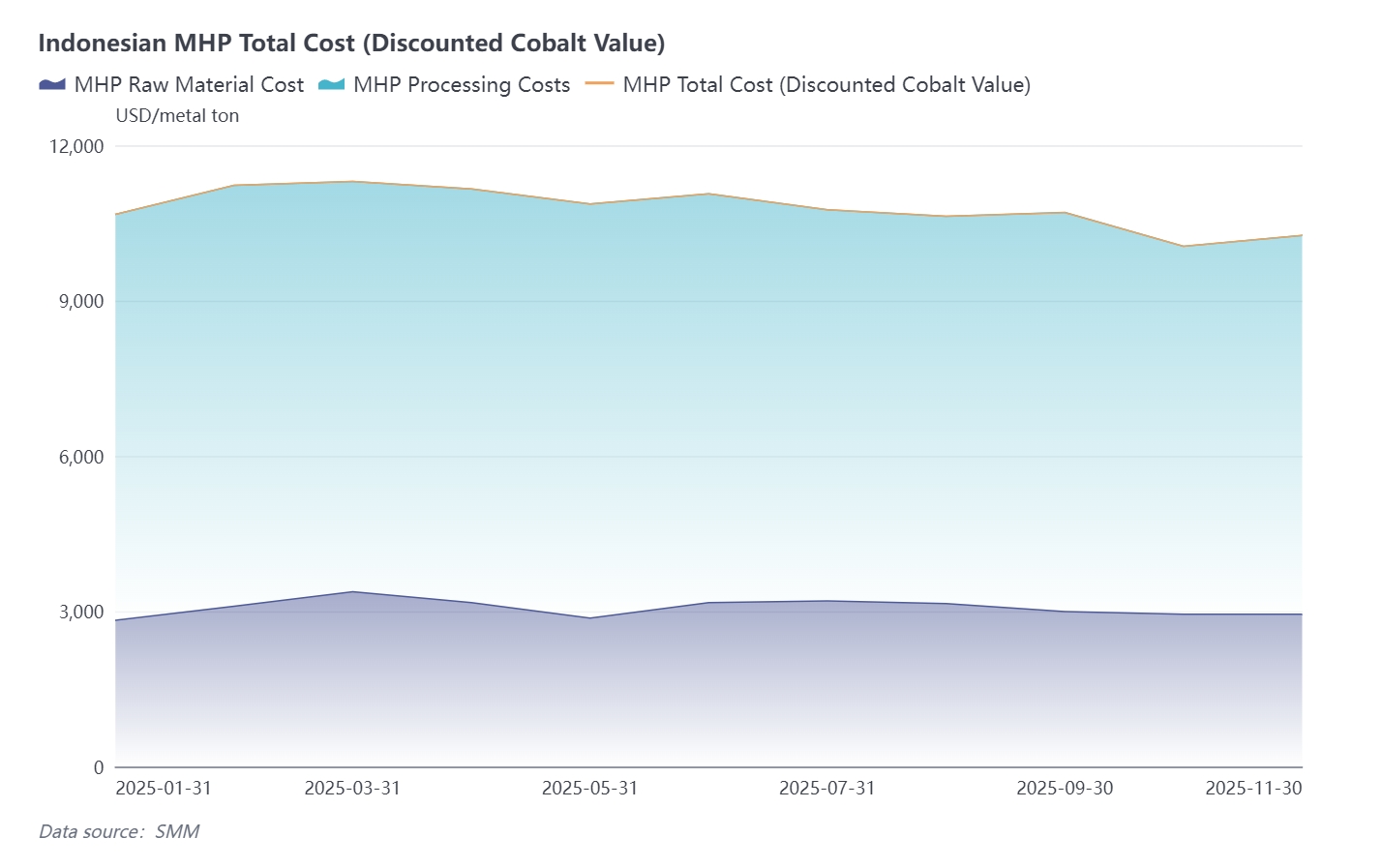

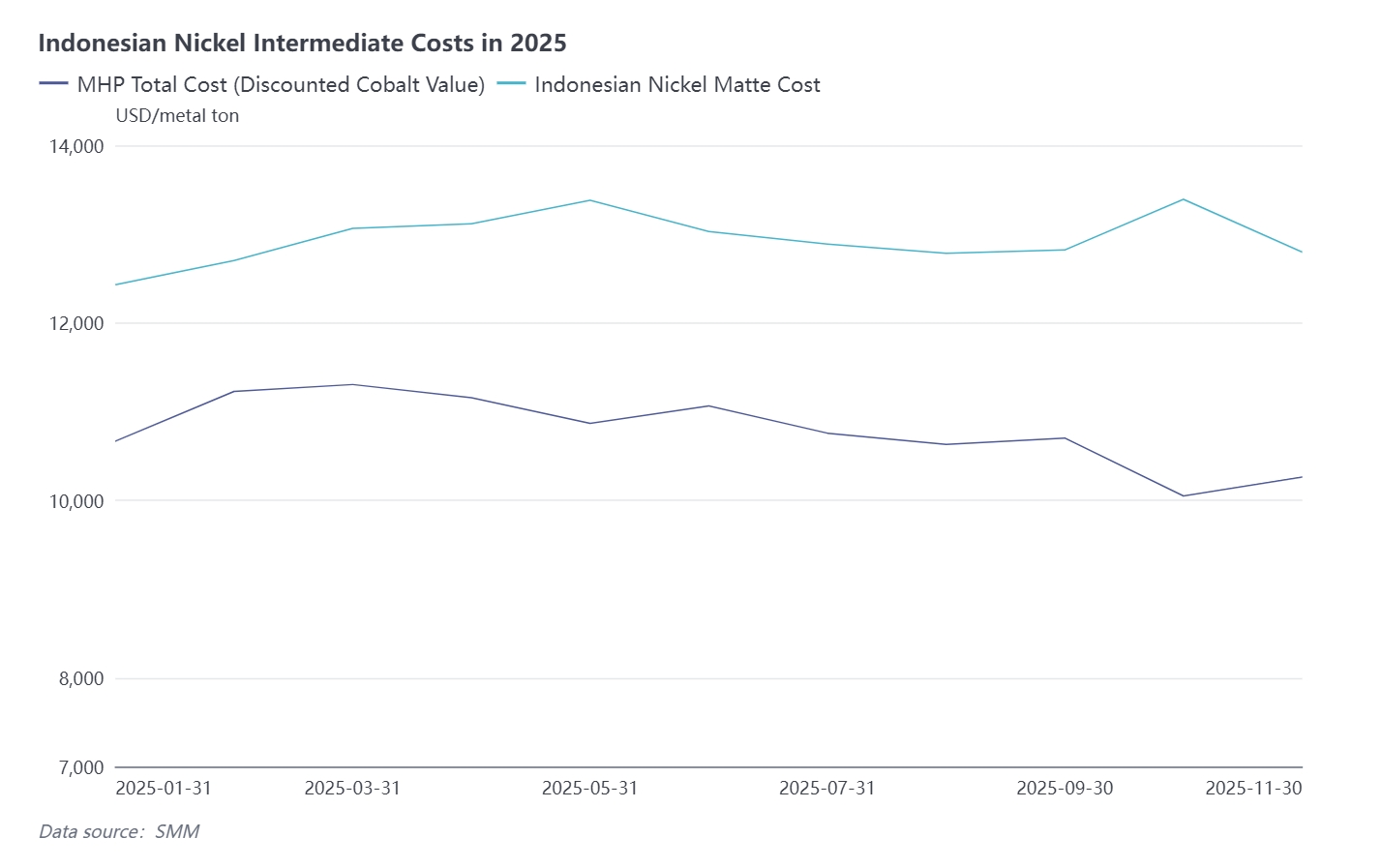

Throughout the year, despite the continuous rise in the price of the auxiliary material sulphur, the production cost of MHP still slightly decreased due to the cobalt discount brought about by the increase in cobalt sulphate prices.

Throughout the year, despite the continuous rise in the price of the auxiliary material sulphur, the production cost of MHP still slightly decreased due to the cobalt discount brought about by the increase in cobalt sulphate prices.

Throughout the year, ore and auxiliary material prices fluctuated frequently, while the production cost of high-grade nickel matte did not show a clear trend.

Throughout the year, ore and auxiliary material prices fluctuated frequently, while the production cost of high-grade nickel matte did not show a clear trend.

Since October, the price of key auxiliary material sulphur has continued to rise, influenced by tightening global supply and growing demand. Supply side, Russia's sulphur export ban took effect on November 2, with the main global sulphur trade sources now being the Middle East, Canada, and Kazakhstan. Demand side, Indonesian smelters continue to stockpile. Looking ahead to December, the tight supply situation is expected to continue supporting sulphur prices, with the market more likely to rise than fall, and the upward trend likely to persist.

Based on the ratio of 11.8 mt of sulphur consumed per mt Ni in MHP production, assuming other factors remain constant, the economics for integrated enterprises using MHP and high-grade nickel matte become basically flat when the sulphur price reaches $637/mt. If the sulphur price exceeds $637/mt, integrated nickel sulphate producers will find it more economical to use high-grade nickel matte as a raw material. When the sulphur price is $690/mt, the production costs of MHP and high-grade nickel matte are equal for integrated enterprises.

V. MHP Cost Structure Breakdown

Nickel ore cost side, with the continuous implementation of Indonesian policies—specifically RKAB, SIMBARA, HPM, and PNBP—restrictions on nickel ore have been imposed in terms of volume, price, and tax, leading to changes in ore prices. From 2022 to the present, the price of 1.2% grade Indonesian laterite nickel ore increased from an annual average of $22.6/mt to $24.5/mt and is expected to continue rising.

Key auxiliary material sulphur side, due to new demand from the new energy sector (iron phosphate and MHP), coupled with new fertilizer demand from Morocco, the growth rate of sulphur supply has failed to keep pace with demand growth. Currently, the sulphur cost for MHP has surpassed the ore cost. Given the significant mismatch between global sulphur capacity distribution and demand distribution, along with international market competition, sulphur prices are expected to continue their upward trend over the next three years, and sulphur cost will remain a major component of MHP cost for the long term.

Next year, MHP hydrometallurgical ore prices and sulphur prices are expected to rise simultaneously, leading to increased MHP costs under the dual impact. In the long term, hydrometallurgical ore prices will be subject to policy controls by the Indonesian government, while sulphur prices will be driven by continuously increasing downstream demand, resulting in a persistent upward trend in MHP production costs.

VI. Outlook for 2026

MHP:

In 2026, Indonesian MHP nickel FOB price is expected to decline throughout the year. Cobalt quota policies in the DRC are creating a cobalt supply gap, which in turn is pushing up cobalt prices. Against this backdrop, the production cost of MHP after cobalt discounting is expected to decrease in 2026, potentially creating room for buyer negotiation. The persistently tight supply situation throughout the year will also support MHP price.

High-Grade Nickel Matte:

In 2026, Indonesian high-grade nickel matte FOB price is expected to rise throughout the year. SMM estimates that the remaining reserves of pyrometallurgical ore in Indonesia can only meet demand for about 10 years. Against this backdrop, Saprolite ore price is expected to rise in 2026, further increasing the cost of high-grade nickel matte and providing support for its price.

Indonesia dominates the production of intermediate products. Leveraging its mineral resource advantages and technological maturity, Indonesia holds the major share of the intermediate products market. From 2021 to 2025, Indonesia's share of global intermediate product supply increased from 22% to 73%. SMM analysis indicates that with the release of capacity from new MHP projects in Indonesia, the country's share of global intermediate product production continues to grow, and its market share is expected to increase further in the future.

![[SMM Analysis] Indonesian nickel ore quota headlines whipsaw China's stainless futures](https://imgqn.smm.cn/usercenter/WNjzM20251217171732.jpeg)